For any non-product related queries, please write to info@perfios.com.

For any non-product related queries, please write to info@perfios.com.

In today's financial landscape, where access to credit can be a game-changer, a revolutionary network is quietly transforming the lending industry. It's called OCEN, short for Open Credit Enablement Network. Imagine this scenario: a 1000 crore worth of loans to be disbursed to 20,000 customers, each seeking an average loan size of 5 lakhs. The cost of acquiring these customers can skyrocket, leading to high interest rates and processing fees for borrowers. But here's where OCEN steps in, simplifying the lending process and lowering the barriers for both lenders and borrowers.

OCEN's origin story is intriguing. It was conceived as a response to the pressing need for a standardized framework in the lending value chain. In a world where data is king, OCEN emerges as the reigning monarch, establishing a universal protocol that ensures lenders and digital platforms speak the same language.

The result? A revolution in how credit is accessed and offered.

At its core, OCEN is more than a common language—it's a credit protocol infrastructure. OCEN contains an API for each step of the lending lifecycle, from application to approval and disbursement. Digital platforms, which until now had a very high barrier to entry for offering financial services, can now seamlessly integrate these APIs as defined in the spec. They can forge connections with multiple lenders, digitize the entire lending process, and extend credit directly on their platforms.

For lenders, OCEN opens a new world of opportunities. They can now open their financial infrastructure to multiple digital platforms, thereby tapping into new pools of borrowers. This expansion of reach and access is unprecedented and transformative.

The result? A win-win scenario for all the participants – digital platforms, lenders, and borrowers.

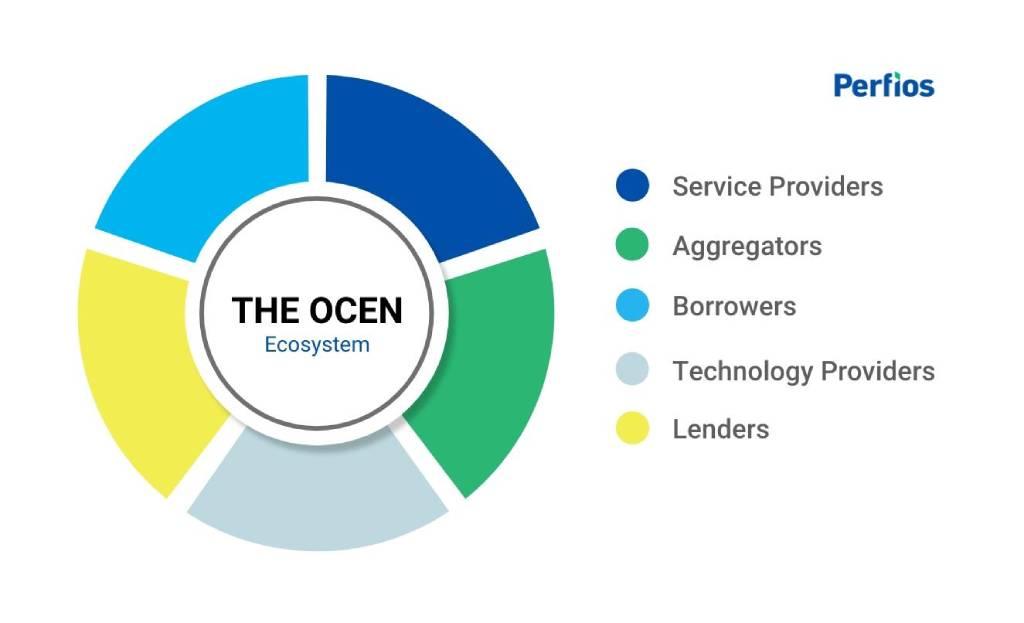

To understand OCEN's transformative potential, it's essential to know the key players within its ecosystem:

These are the customer-facing digital platforms, with a core offering to those customers, that can source borrowers. Think of giants like Zomato and Amazon, armed with a treasure trove of data like turnover, rating, TAT, product range, inventory, etc., about the businesses they interact with. They can augment their product offering by originating and enabling credit on their platform itself. Loan Service Providers (LSPs) can leverage their digital platforms to introduce the option to avail credit across products like personal loans, business loans, BNPL, Credit Cards, Credit Limits, etc.

An Account Aggregators (AA) is a type of RBI-regulated entity that helps an individual securely and digitally access and share information from one financial institution they have an account with to any other regulated financial institution in the AA network. These regulated entities simplify the sharing of financial data securely and digitally. Instead of navigating the maze of paperwork, borrowers can grant consent to share their data with lenders for assessment. This streamlined process minimizes user effort, saves time, reduces costs, and eliminates data manipulation risks.

Technology Service Providers are FinTech companies like Perfios, Lentra, TransUnion, and Crisil that work closely with lenders and platforms to integrate OCEN seamlessly. They play a pivotal role in onboarding and tailoring credit programs. This segment can also be denoted as embedded finance providers.

Banks, NBFCs, and small finance banks provide the capital and core banking networks necessary for OCEN's success.

Whether they are MSMEs or individual consumers, borrowers gain access to formal & affordable credit. They also benefit from the secure and fully digital credit options available through LSP platforms.

The emergence of OCEN couldn't have been more timely. It addresses significant challenges faced by lenders when operating on digital platforms:

The high cost of acquiring customers for small-ticket loans often results in elevated interest rates and processing fees. OCEN streamlines the process, reducing costs for both lenders and borrowers. For instance, disbursing a total loan of, say, 1000 crores, would typically require acquiring 20,000 customers with an average ticket size of 5 lakhs. This process involves substantial expenses, resulting in higher interest rates and processing fees for borrowers. OCEN's standardized protocol lowers the acquisition cost, making credit more accessible.

OCEN simplifies data collection and verification, ensuring lenders have the insights they need. Lending to MSMEs digitally demands a clear set of data for accurate assessment and pricing. This includes data on turnover, account statements, GST returns, and more. In the past, collecting and verifying this data was a major challenge for lenders. OCEN's standardized framework streamlines this process, providing lenders with the rich data signals they require for accurate decision-making.

In the world of lending, timing is everything. Money required today may not be the same as money required tomorrow. In many cases, insufficient or unclear data can lead to lengthy assessment processes, resulting in a poor customer experience. Borrowers may turn to more expensive sources of financing or remain underfinanced, which can ultimately impact their businesses. OCEN's streamlined approach addresses this challenge, ensuring that borrowers get timely access to the credit they need.

Let's illustrate how OCEN works in practice. Consider “X”, a restaurant aggregator, and “ABC'' Bank:

- “X”, armed with extensive data on restaurants, initiates the distribution of credit to restaurant owners.

- Restaurant owners see loan options available to them on their regular business platform & can choose to avail just when they need it.

- Through OCEN's APIs, “X” shares essential information about the borrower with “ABC” Bank.

- Account Aggregator steps in with the customer's consent, sharing relevant data like account statements and GST returns.

- Technology Service Providers assist in data assessment.

- Loan terms are set, and the loan is disbursed seamlessly.

- “X” aids in servicing the loan, ensuring timely repayments.

This example showcases the power of OCEN in action. The same journey might also involve multiple banks and NBFCs to provide multiple loan offers to the borrowers. OCEN streamlines the selection process by aiding the borrower to pick the most optimal offer through their framework.

By connecting digital platforms, lenders, and borrowers through a standardized protocol, OCEN simplifies lending, reduces costs, and accelerates access to credit. It's a win for all parties involved, creating a thriving ecosystem where businesses and individuals can access the financial support they need.

The Open Credit Enablement Network (OCEN) is revolutionizing the lending industry, making it easier and more accessible for everyone. With OCEN, businesses like Zomato and Amazon can offer financial services, benefiting both lenders and borrowers. Account Aggregators simplify data sharing, while Technology Service Providers ensure everything runs smoothly behind the scenes. Traditional lenders and small businesses can now tap into a world of opportunities with OCEN.

As we look to the future, it's clear that OCEN is a game-changer. It simplifies lending, reducing costs, and speeding up processes. However, the true power of OCEN lies in its potential to transform the lives of countless small businesses and individuals by providing easier access to credit.

Stay tuned for our next blog where we’ll deep dive into the capabilities of OCEN and how it will soon leapfrog over traditional credit ecosystems.

Perfios Software Solutions is India’s largest SaaS-based B2B fintech software company enabling 900+ FIs to take informed decisions in real-time. Headquartered in mumbai, India, Perfios specializes in real-time credit decisioning, analytics, onboarding automation, due diligence, monitoring, litigation automation, and more.

Perfios’ core data platform has been built to aggregate and analyze both structured and unstructured data and provide vertical solutions combining both consented and public data for the BFSI space catering to their stringent Scale Performance, Security, and other SLA requirements.

You can write to us at connect@perfios.com

For more Such information contact us @ https://solutions.perfios.com/request-for-demo