For any non-product related queries, please write to info@perfios.com.

For any non-product related queries, please write to info@perfios.com.

Within the dynamic realm of Indian finance, a profound transformation is unfolding, poised to redefine the very foundations of the credit landscape. This transformation is embodied by the Open Credit Enablement Network (OCEN), an innovative API framework designed to reshape credit access across the spectrum of businesses.

Let’s not forget the vast chasm of India's credit gap—a challenge that demands collaborative efforts from the public and private sectors. OCEN stands at the precipice of this challenge, aiming to remove the credit gap and enable the flow of affordable credit to those who need it the most - India’s small businesses & individuals who can power their aspirations.

Birthed by the minds at iSPIRIT and announced at the Global Fintech Festival in 2020, the promise of OCEN goes far beyond its technical framework! OCEN brings together regulatory agencies, banks, NBFCs, fintech entities, marketplaces, and most crucially, the unsung heroes of the economic ecosystem — small business owners and individuals — towards a reimagined superior credit ecosystem.

Stepping into the future, the ambition is clear: scale this cutting-edge API framework to encompass hundreds of thousands, and eventually millions, of small businesses and individuals.

In this article, we embark on a journey to unravel OCEN's disruptive potential which can be yoked by Loan Service Providers (LSPs), Technology Service Providers (TSPs), and lenders to extend their services to borrowers. Prepare to delve into its unfolding narrative which holds the potential to reshape India's economic trajectory for an inclusive, resilient financial future.

In the intricate labyrinth of credit, challenges that once seemed insurmountable now stand at the precipice of transformation. The credit ecosystem, a foundational pillar of India's economy, grapples with a paradox—limited accessibility. MSMEs and small-ticket borrowers, the driving forces behind economic growth, are hindered by stringent credit prerequisites and convoluted application processes.

The echoes of the global financial crisis still reverberate, underscoring the urgency of robust credit risk management. Yet, even as organizations endeavor to refine their credit risk assessment strategies, they are met with formidable obstacles—inefficient data management, fragmented risk modeling infrastructure, complex risk tools, and underwhelming reporting mechanisms because of which the need to find a solution to these roadblocks has become crucial.

Enter OCEN—an audacious force heralding a new era of credit dynamics!

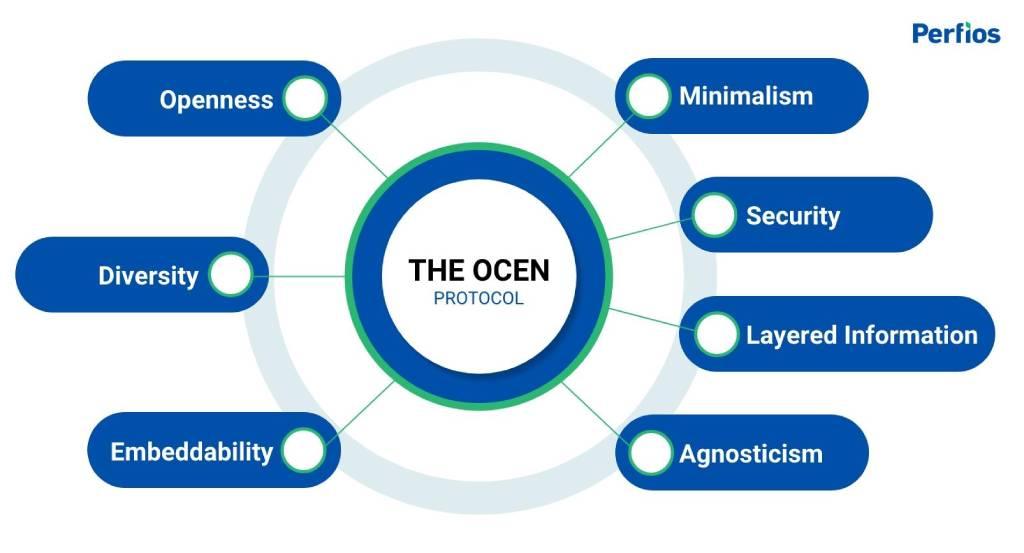

At its core, OCEN presents a visionary open API framework poised to bridge the gap between borrowers and lenders and hence promoting diversity along the lending chain. OCEN envisions a world where secure intra-day or inter-day loans serve as lifelines for individual proprietors and micro, small, and medium enterprises (MSMEs) navigating cash flow challenges. OCEN's essence radiates through the digital minimization of the loan lifecycle, igniting origination, underwriting, and servicing processes that seamlessly connect platforms, marketplaces, and financial institutions. This is made possible by the embeddable platform which is built through layered information stacked on top of India’s transformative Digital Public Infrastructure, i.e. the identity layer (Aadhar), Payments Layer (UPI) and the Data Empowerment layer (DEPA).

India's MSME sector, a resilient contributor to the GDP, stands as a testament to determination amidst credit complexities. While MSME-related products command a significant 48% share in India's exports, as per a report on OCEN by Invest India, merely 11% of these enterprises navigate the intricate maze of credit channels presented by traditional lenders.

OCEN's narrative reframes this story. Its promise of immediate liquidity breathes vitality into cash-strapped MSMEs and individual proprietors, unlocking a spectrum of benefits.

The once-marginalized 89% of borrowers now stand on the brink of financial empowerment and OCEN heralds an era of financial inclusion. The exorbitant interest rates wielded by non-banking financial companies (NBFCs) and loan sharks arising due to lack of quality data will recede, paving the path for accessible credit.

By discerning correlations between purchasing behavior and repayment habits,i.e., creditworthiness, OCEN empowers lenders to make informed decisions. It nurtures a dynamic lending landscape that adapts to the ebb and flow of business realities. OCEN's data-driven approach extends beyond individual transactions; it equips lenders to gauge market trends, anticipate shifts in consumer behavior, and promptly respond to economic fluctuations.

MSMEs and individuals thrive on tailored solutions and bespoke loans to leverage cash flows; OCEN dismantles the notion of unprofitable smaller loans. MSMEs now possess the capacity to scale endeavors with this infusion of liquidity transcending individual enterprises to cascade into a holistic economic ecosystem.

"There is something now which is getting developed called the open credit enablement network or OCEN which allows you to connect lenders to marketplaces...and this essentially acts as a common language, between lenders and borrowers."

-Nandan Nilekeni

India's digital lending landscape teeters on the cusp of metamorphosis, and experts predict OCEN to take center stage. Forecasts predicting market growth to $100 billion by 2023 underscore the winds of transformation that it will usher in. A substantial segment of the population, comprising over 300 million individuals, remains untapped by formal credit avenues, engendering a substantial credit gap of $250 billion. OCEN will navigate this terrain, harnessing the digital transaction history amassed by the recently digitized user base.

Yet, as OCEN's potential shines, we must also recognize the challenges that the participants in this ecosystem should address.

A foreseeable surge in borrowers could bring about a concerning rise in loan defaults, demanding vigilant risk management. Alongside the boon of data availability, concerns for privacy and safeguarding personal information beckon. In the digital era, cyber threats amass like dark clouds on the horizon underscoring the urgency for fortified firewalls and strong cybersecurity strategies.

As we set sail into this uncharted territory, these challenges become part of OCEN's narrative—a story of transformation illuminated by both triumphs and trials. By recognizing these potential drawbacks and addressing them head-on, OCEN's transformative journey can be guided towards a secure credit landscape.

As OCEN propels India toward credit democratization and financial inclusivity, a new era emerges. This technology-driven transformation pledges an era where small businesses and individuals flourish, fortifying the Indian economy and reshaping the nation's financial trajectory.

OCEN's disruptive impact is already evident, creating pathways for small businesses, entrepreneurs, and traders to thrive. It serves as a testament to the power of innovation while exemplifying the collaborative spirit required to navigate the evolving financial landscape. By embracing change, leveraging partnerships, and harnessing OCEN's potential, LSPs, TSPs, lenders and borrowers can together usher in a ripple effect of credit accessibility that can scale India’s growth.

For a deeper understanding of the topic, tune into our next blog in the series where we will be unlocking the various features and facets of OCEN.

Perfios Software Solutions is India’s largest SaaS-based B2B fintech software company enabling 900+ FIs to take informed decisions in real-time. Headquartered in mumbai, India, Perfios specializes in real-time credit decisioning, analytics, onboarding automation, due diligence, monitoring, litigation automation, and more.

Perfios’ core data platform has been built to aggregate and analyze both structured and unstructured data and provide vertical solutions combining both consented and public data for the BFSI space catering to their stringent Scale Performance, Security, and other SLA requirements.

You can write to us at connect@perfios.com

For more Such information contact us @ https://solutions.perfios.com/request-for-demo