For any non-product related queries, please write to info@perfios.com.

For any non-product related queries, please write to info@perfios.com.

In the heart of India's bustling economy, the MSME sector faced a formidable challenge – a challenge that threatened the very essence of entrepreneurship and financial stability. The stark reality of 85% of the MSME lending being underserved, coupled with an astounding credit gap of 17 trillion rupees, has been a constant reminder of the limitations of our current lending landscape.

The challenges that have long plagued the MSME sector have not only been hurdles for entrepreneurs but also for lenders like XYZ Bank which are deeply rooted in the intricacies of the financial world. Come 2023, lenders like XYZ Bank that service loans to MSMEs stand at the precipice of a transformative journey thanks to the latest versioning of the Open Credit Enablement System (OCEN) 4.0.

The crux of the problem lies in the disparity between the traditional lending norms and the unique needs of these micro, small, and medium-sized enterprises (MSMEs). Their lack of stable income, coupled with the impracticality of small sachet loans, created a daunting barrier, stifling their growth potential. For lenders, the dilemma was equally daunting – how to bridge this gap efficiently while adhering to regulatory norms (i.e., acquisition costs, underwriting, loan processing & disbursement, managing collections, and overhead charges), especially in a landscape where the risk was high, and margins were thin.

OCEN 4.0 emerges as a game-changer, offering XYZ bank an opportunity to find new solutions to this. XYZ bank recognizes that OCEN 4.0 is not just a technological upgrade from its previous pilots; it's a lifeline for lenders to enhance the existing credit system.

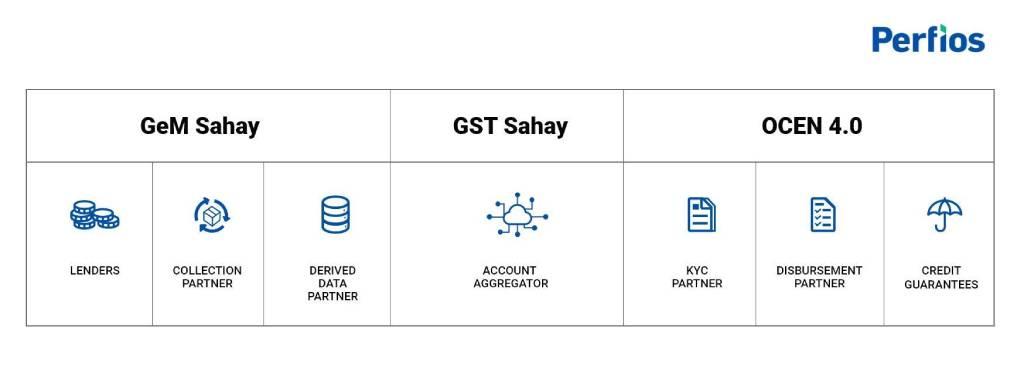

● May 2021 - The GeM Sahay pilot comes into play which allows small-ticket loans of a smaller tenure enabled by the OCEN framework.

● Jan 2023 - The launch of the GST Sahay pilot which enabled the disbursement of loans using GST data, Account Aggregators, and the Digital Lending Guidelines set by the Reserve Bank of India(RBI)

The traditional barriers that hindered MSMEs from accessing long-term loans due to unstable incomes and low credit scores are now dismantled. OCEN's innovative approach, especially the introduction of the Products Registry and enhanced collaboration frameworks within the Products Network along with other updates to its API specs, revolutionizes how XYZ bank engages with potential borrowers. These features not only simplify the lending processes but also create a dynamic ecosystem where lending becomes more agile and tailored to the specific needs of the MSMEs.

What truly sets OCEN 4.0 apart is its ability to harness high-provenance data in lieu of Derived Data Partners (DDP), enabling XYZ Bank to delve into the realm of small sachet loans with confidence. In the past, the impracticality of these loans due to low return margins was a significant concern. However, OCEN's digital prowess, coupled with its emphasis on financial inclusion, empowers XYZ Bank to navigate this landscape effectively. The integration of regulatory operations into this digital framework ensures that lending practices are not only innovative but also compliant, a vital aspect of any lender’s operations.

The streamlined processes, collaborative networks, and refined API specifications not only enhance lending efficiency but also help the lender to expand their horizons. This innovation enables XYZ Bank to transcend previous limitations, embracing a future where lending isn't just a transactional process but a catalyst for sustainable growth. With OCEN 4.0, XYZ Bank finds itself at the forefront of a lending revolution, ready to support and empower lending in the MSME sector like never before!

Enter OCEN 4.0, a revolutionary force in the financial sphere built on the incremental improvements of the previous pilots, GeM Sahay and GST Sahay. At its core, OCEN addresses the crux of the problem by redefining lending norms and making financial inclusion more than just a buzzword. Here’s what is new and improved with the latest updates to OCEN’s specs:

One of its primary innovations is the introduction of the Products Registry, a dynamic platform that allows lenders to create tailor-made financial products. This means that the age-old one-size-fits-all approach to lending has become obsolete. Lenders can now craft solutions that align precisely with the unique needs of MSME lending, ensuring that financial support isn't just accessible but also customized.

Additionally, OCEN 4.0 has dismantled the barriers around small sachet loans like never before through the introduction of specialized roles and enhanced data processing. Through the recent versioning’s advanced data analytics and digitized cash flow mechanisms, lenders can now confidently venture into the realm of small-scale lending with better standardization provided by KYC partners. High-provenance data equips lenders with the insights needed to assess risk accurately and offer smaller loans with confidence. This move from a risk-averse approach to a data-driven, nuanced understanding of lending not only empowers lenders but also opens doors for MSMEs that were previously considered too risky to support.

Furthermore, the collaborative networks established within the Products Network ensure that lenders, MSMEs, and regulatory bodies work in harmony. The burden of compliance and regulatory operations is alleviated through the specialized roles defined within the OCEN framework. This ensures that the lending process is not only efficient but also compliant with the stringent norms set by regulatory bodies.

In a groundbreaking move, the new reveal of OCEN 4.0 showcased an auction-based loan bidding model. Under this new model, each loan application is shared with multiple lenders creating a competitive marketplace. This mechanism helps in the regulation of the market and ensures that lenders process applications swiftly and offer attractive terms, ensuring that borrowers receive the help that they need.

In the transformative landscape of Indian finance, OCEN 4.0 is rewriting the rules of lending allowing tailored financial solutions for individual businesses & fostering inclusivity and customization. Addressing the longstanding challenges, it dismantles barriers with specialized roles like product registries and Product Networks, while the introduction of an auction-based model has fostered a competitive marketplace.

Looking ahead, the roadmap for OCEN envisions real-time regulation for audits and provisions for specialized disbursement and escrow-based collections. iSpirit has also declared that the standardization of loan labeling in the auction-based model will streamline the financial future, ensuring fairness and efficiency in MSME lending practices. OCEN 4.0 not only marks a turning point but also heralds a future where financial inclusion, innovation, and compliance converge for the betterment of India's thriving MSME sector.

Perfios Software Solutions is India’s largest SaaS-based B2B fintech software company enabling 900+ FIs to make informed decisions in real-time. Headquartered in Mumbai, India, Perfios specializes in real-time credit decisioning, analytics, onboarding automation, due diligence, monitoring, litigation automation, and more.

Perfios’ core data platform has been built to aggregate and analyze both structured and unstructured data and provide vertical solutions combining both consented and public data for the BFSI space catering to their stringent Scale Performance, Security, and other SLA requirements.

You can write to us at connect@perfios.com

For more Such information contact us@ https://solutions.perfios.com/request-for-demo