For any non-product related queries, please write to info@perfios.com.

For any non-product related queries, please write to info@perfios.com.

Over the past couple of decades credit cards, EMI cards, eNACH and to a certain extent EMI-on-debit cards have tried to become the go-to instrument for “Credit at the point of consumption”.

Though almost all of them have failed to realize this expectation. EMI cards did really well, but they faced the same limitation as the credit card or EMI-on-debit card did i.e. lack of acceptance by merchants, lack of awareness and the general mistrust in credit.

In recent years credit cards and other credit instruments seem to be gaining traction and the introduction of “Credit on UPI” seems to be a step in the right direction when it comes to making credit accessible to passes.

Here is a deep dive into where credit cards stand and what the future looks like for Credit on UPI. We cover,

- Why Credit cards and Debit cards didn’t work?

- Rise of EMI Cards

- Credit on UPI, what to expect.

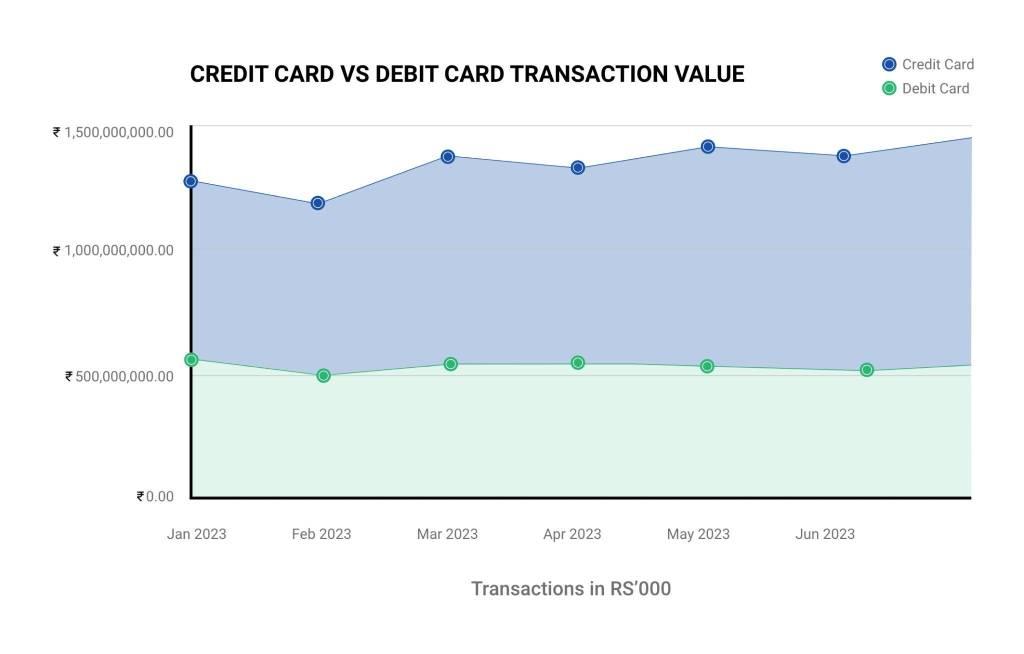

As of April 2023, 8.9 crore1 credit cards are in circulation, slated to reach 10 crore cards by end of this year. Alternatively, debit cards have seen much better acceptance with over 97 crore debit cards1 in circulation at the time of writing this article.

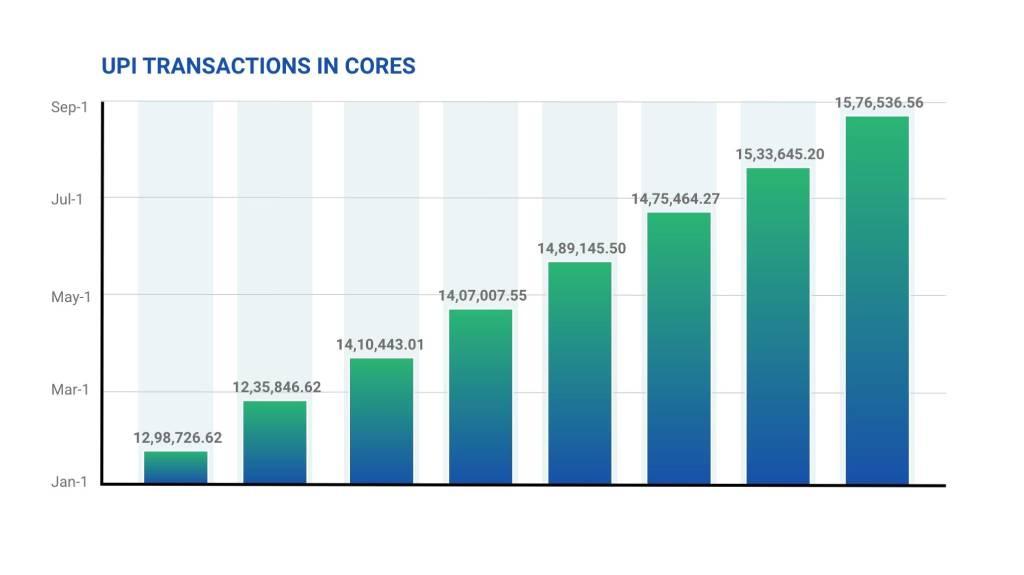

UPI, on the other hand, has seen an unprecedented speed in adoption across the country. Fueled by demonetization and pandemic, UPI as of 2023 has 30 crore users and 5 crore merchants2 onboarded.

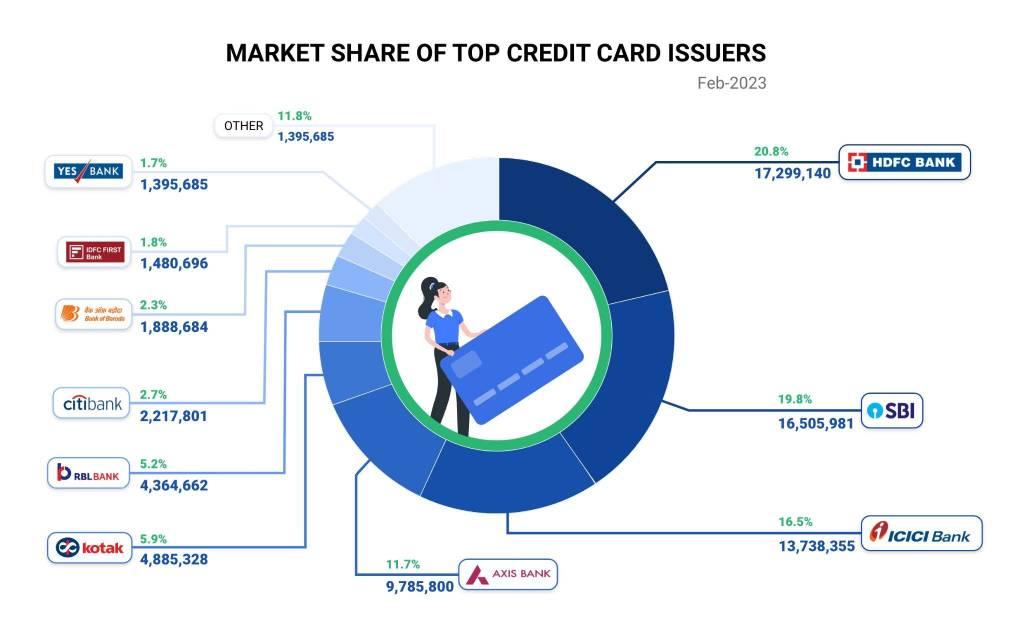

From the banking side of things, 484 financial institutions in India support UPI7 while most of the credit card market is dominated by top 4 banks.

At one point, credit cards were supposed to be the instrument that would allow consumers to gain access to credit at the point of consumption faster than a loan and would give underserved consumers an opportunity to access credit.

Over the years, credit cards failed to gain as much traction as one would have imagined considering how lucrative it is for banks and how easy it was to use for consumers.

The very first credit card was issued by the Central Bank of India back in the 1980s, followed by Andra bank.

But the anti-credit sentiment combined with general distrust among the consumers and merchants unwillingness to get a PoS system or pay for transactions meant low adoption.

From a credit perspective, first NACH followed by eNACH and then debit card EMIs tried to do what credit cards couldn’t, i.e. become the go- to credit at the point of purchase instrument for consumers and more importantly give credit access to millions of underserved consumers.

In recent years credit card usage has been steadily increasing. Backed by fintechs, demonetisation, pandemic, ecommerce merchants, and a growing middle class with disposable income, we are actually seeing an uptake in CC usage, even overtaking DC usage in 20234.

Having said that, credit cards and EMI on Debit cards, which were supposed to be the go to credit instruments for credit requirements of < INR 5000, never reached their potential. Here is why:

Most activated credit card customers tend to cost anything around INR 3000 to INR 5000 in CAC for the bank.

Banks tend to shy away from small ticket credit requirements considering the time it takes to actually get back the money that is lent to the customer. Anything less than 50,000 usually becomes expensive for the banks to actually consider.

This is especially true in the case of new customers. Most credit card companies tend to sell to existing bank customers, where customer onboarding is already done, because the risk is lower and CAC is manageable.

This takes us to the second reason why CCs haven’t taken off.

Most credit card companies tend to sell to their existing bank customers instead of new customers.

Risk associated with giving a credit instrument to new customers and the lack of financial data to actually know if they would pay back the loan meant most banks could never scale their credit card business beyond existing bank customers.

CIBIL solved it at some point, though that just meant companies sold to customers who already had existing credit cards.

In the case of the mid to low income segment, this gets worse. The lack of credible financial data means that most banks and NBFCs tend to shy away because of the risk involved in lending to these consumers.

From consumers' perspective, they could only use credit cards and debit cards at merchants who had a PoS.

India has more than 8.1 million PoS1 deployed. Though a really good number, most customers in tier 2 and tier 3 cities would rarely have access to merchants that use a PoS.

The only other way they could use CC or EMI on DC as a credit instrument would be via ecommerce websites, which have about 125 million users in total.

The rest who do not have access to merchants with PoS or those who do not prefer ecommerce transactions would not be able to use these instruments, even if they had the credit history eligible for it.

Another reason why CC and DC haven’t been able to take off is because of the mostly negative image the credit has.

Even when a consumer looks at getting a credit card, there is not enough data on which type of credit or debit card would be good for them based on their financial profile and requirements.

Combine this with the general lack of financial education among the consumers, means most continue to see credit in a negative light.

When talking about short term credit or loans for purchases i.e. “Credit for consumption” usually refers to using credit card EMI, debit card EMI, Bajaj EMI card, and at some places eNACH.

While the credit card penetration is low and EMI via debit cards hasn’t done as well as we thought it would. The clear winner has been the EMI cards; specifically Bajaj EMI cards.

A recent study by HomeCredit 3 found that 50% of Gen Z borrowers preferred EMI cards for purchases followed by credit card and then BNPL instruments.

EMI cards like Bajaj Finserv EMI cards were able to do what CC and DCs couldn’t, driven by merchants and ecommerce companies, they have become the preferred mode of payment for “Credit at point of consumption” purchases.

However, it is still limited mostly to electronics and other consumer durables and in a way limited to people looking to make those purchases either via EMI card enabled merchants or ecommerce stores like Flipkart and Amazon.

This also meant there was barely any relevance outside high value consumer goods.

Considering the challenges that CC and DC faced in getting the credit line for low-medium income groups, especially in <50,000 type of credit groups.

Credit on UPI, with its access and acceptance across consumers and merchants, looks like the instrument that could bridge the gap between banks and consumers with lower value credit requirements.

Before we dig deeper into this, here is a short history lesson on UPI.

UPI at its core is a system that connects multiple bank accounts of a user to a single application powering peer-to-peer payments, merchant payments and fund routing through it.

What started with 12 banks on a pilot launch now has over 458 banks active on the interface, allowing 30 crore users and 5 crore merchants on it.

Over the last few years, UPI has grown 40-50% year-on-year, a staggering deviance from the credit and EMI on debit cards. This not only shows acceptance but the trust that the general public has on UPI as a platform.

Backed by NPCI, RBI and helped by the advent of fintech startups like Paytm, PhonePe and BharatPe, acceptance of UPI as a payment mode has been nothing short of amazing.

Credit line on UPI solves 2 major problems of

1. Acceptance and

2. Awareness among the low-mid income groups.

Acceptance of UPI as payment mode is evident from the sheer number of users on UPI, which for one, UPI has far more users, banks and merchants on it than DC and CC combined.

Second, it is growing exponentially even now. For example, in 2022-23 alone UPI grew 115% in volume6.

Apart from the what Credit on UPI for the consumers, here is what Credit-on-UPI can do for lenders:

Pre-onboarded app customers means players like Gpay and Paytm have an opportunity to give credit lines directly from their UPI apps minus the cost associated with giving out a credit card.

Banks, on the other hand, can partner with these players to offer smaller low risk credit limits to gauge payment behavior leading to an option to onboard customers to larger credit lines and even credit cards over time.

UPI acceptance across consumers and merchants would also lead to faster onboarding and usage by consumers.

One of the major reasons why credit card companies tend to only sell to ETB customers is their appetite for risk. Which in a way has been positive behavior.

On the other hand, this was the case due to lack of financial data in case of low-to-mid income groups that could be used to check credit worthiness of the consumers.

UPI data combined with access to this data via AA means that banks partnered with UPI apps can make instant decisions on the credit worthiness of customers without an extensive financial history for erstwhile NTB customers.

Access to this data via AA and access to customer UPI also means that now banks can start with a small, say < INR 5,000, credit line and monitor repayment behavior before actually giving out larger credit lines.

This also means the financial data can be used to create custom offers both in credit cards and credit to the customer based on their financial behavior. All of this combined will drive acceptance and would improve activation rates.

While there are quite a few things that banks and fintech players can do with UPI and credit-on-UPI, the actual opportunity lies in getting NTB customers into the formal credit system.

Credit-on-UPI has the potential to not only grow the existing lending business but also into its gambit the large underserved populace from tier 2 and tier 3 cities.

My hope is that credit-on-UPI is able to do what credit cards couldn’t. For now though, the odds are in its favor, especially when considering how UPI itself has grown across the board.

Perfios Software Solutions is India’s largest SaaS-based B2B fintech software company enabling 900+ FIs to take informed decisions in real-time. Headquartered in Bangalore, India, Perfios specialises in real-time credit decisioning, analytics, onboarding automation, due diligence, monitoring, litigation automation, and more.

Perfios’ core data platform has been built to aggregate and analyse both structured and unstructured data and provide vertical solutions combining both consented and public data for the BFSI space catering to their stringent Scale Performance, Security, and other SLA requirements.

You can write to us at @ connect@perfios.com

For more such information @ https://solutions.perfios.com/request-for-demo