For any non-product related queries, please write to info@perfios.com.

For any non-product related queries, please write to info@perfios.com.

● An insight into GenZ world of engaging via mobile apps for financial transactions

● Reserve Bank of India’s (RBIs) Regulatory Framework for financial services

● Mobile banking compliance in India and things you need to know

● Ways of designing user-friendly and 100% compliant mobile banking apps

Ever noticed how our smartphones have turned into mini-banks?

Gone are the days of waiting in long queues or filling out endless forms. Today, a few taps on our screens, and voila! Banking done. It's the age of convenience, and mobile banking apps are leading the charge.

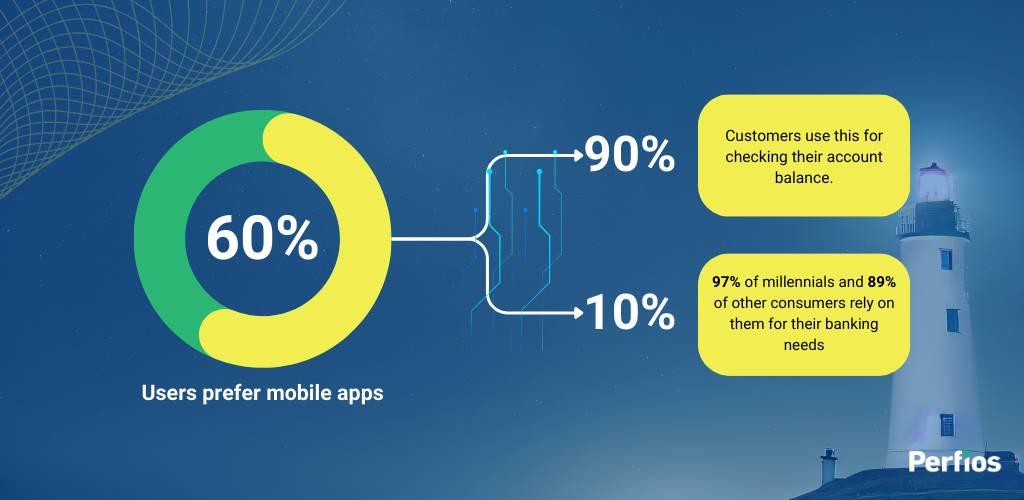

Mobile banking apps are becoming increasingly popular, with 60% of users preferring them over websites. A notable 90% utilize these apps to check account balances, while 97% of millennials and 89% of other consumers rely on them for their banking needs. Their 24/7 accessibility, ease of use, and robust security measures contribute to this growing preference, facilitating a variety of financial tasks right at the users' fingertips.

But here's the thing. As we embrace this digital shift, there's a crucial behind-the-scenes process that needs some spotlight: onboarding. It's not just about signing up; it's the first dance between the user and the bank's app. And trust me, first impressions matter!

Now, diving into the nitty-gritty, onboarding isn't just about user experience. It's a tightrope walk of ensuring compliance. Banks have a hefty rulebook to follow, especially when welcoming new users. Top of the compliance list? KYC (Know Your Customer) and AML (Anti-Money Laundering) rules. These aren't just fancy acronyms; they're the backbone of secure banking, ensuring that you signing up is indeed you and not someone with dubious intentions.

So, what's in store for this blog? We're about to embark on a journey, unraveling the maze of mobile banking onboarding. From the importance of identity checks to the maze of rules banks need to follow, we'll break it all down.

Financial institutions, including banks offering mobile applications, are subject to a complex web of regulatory requirements aimed at safeguarding the financial system and protecting consumers. This section will delve into the key aspects of the regulatory framework that banks must navigate when onboarding customers via mobile applications.

KYC (Know Your Customer) RegulationsKYC regulations require banks to verify the identity of their customers to prevent fraud, money laundering, and terrorist financing. It entails collecting and verifying customer information, including name, address, and identification documents. |

AML (Anti-Money Laundering) LawsAML laws are designed to detect and prevent money laundering activities within the banking system. These laws mandate the establishment of robust anti-money laundering programs, customer due diligence, and reporting of suspicious transactions. |

CDD (Customer Due Diligence) Requirements:CDD is a fundamental component of AML regulations, necessitating that banks understand the nature of their customers' businesses, assess the risk they pose, and continuously monitor their activities. |

FATF (Financial Action Task Force):The FATF is an intergovernmental organization that sets international standards and promotes measures for combating money laundering and terrorist financing. Its recommendations serve as a global benchmark for AML and CDD practices. |

OCC (Office of the Comptroller of the Currency):In the United States, the OCC is a key regulatory body overseeing national banks and federal savings associations. It provides guidelines and regulations on various aspects of banking, including customer onboarding and risk management. |

GDPR (General Data Protection Regulation):While primarily focused on data protection and privacy in the European Union, GDPR has a significant impact on how banks handle customer data worldwide. It mandates stringent data protection practices and consent requirements. |

Compliance with these regulations is not optional for banks; it's a legal and ethical imperative. Non-compliance can lead to severe penalties, damage to reputation, and legal repercussions. Thus, banks must invest in robust compliance programs and technologies to meet the ever-evolving regulatory requirements.

Mobile apps are becoming the primary interface for customer interactions. Ensuring compliance with regulatory requirements is not limited to paperwork and procedures—it extends deeply into the realm of mobile app development, including the Onboarding Customer API. This section will explore the crucial aspects of developing a mobile banking application that not only provides an excellent user experience but also aligns seamlessly with compliance standards through an effective Onboarding Customer API.

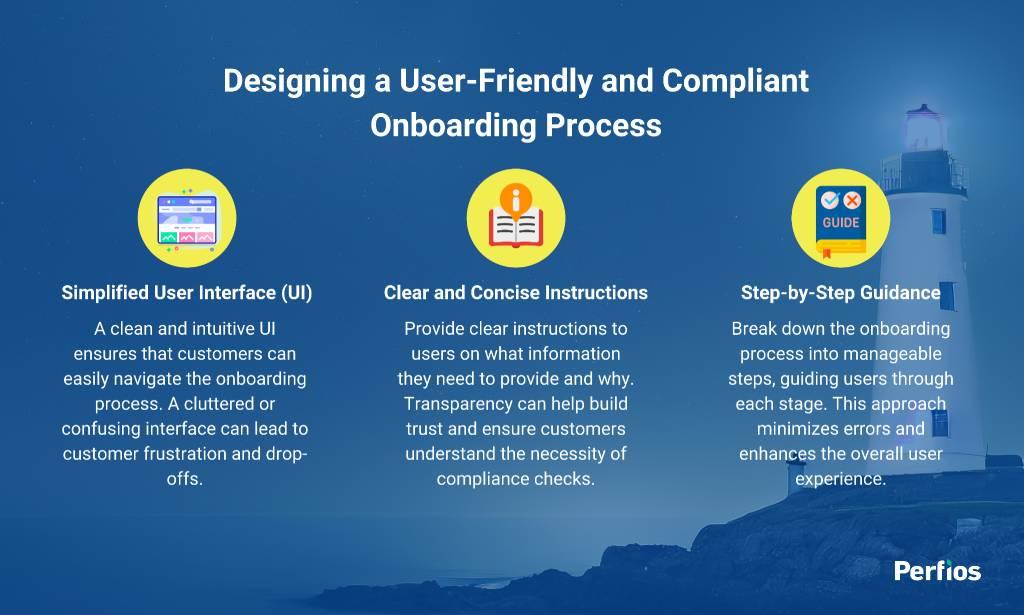

A user-friendly onboarding process is the cornerstone of a successful mobile banking application. However, it must also adhere to compliance standards. Here are some key considerations:

In this regard, Perfios provides 100% compliant mobile app onboarding solutions, ensuring a frictionless yet compliant user journey.

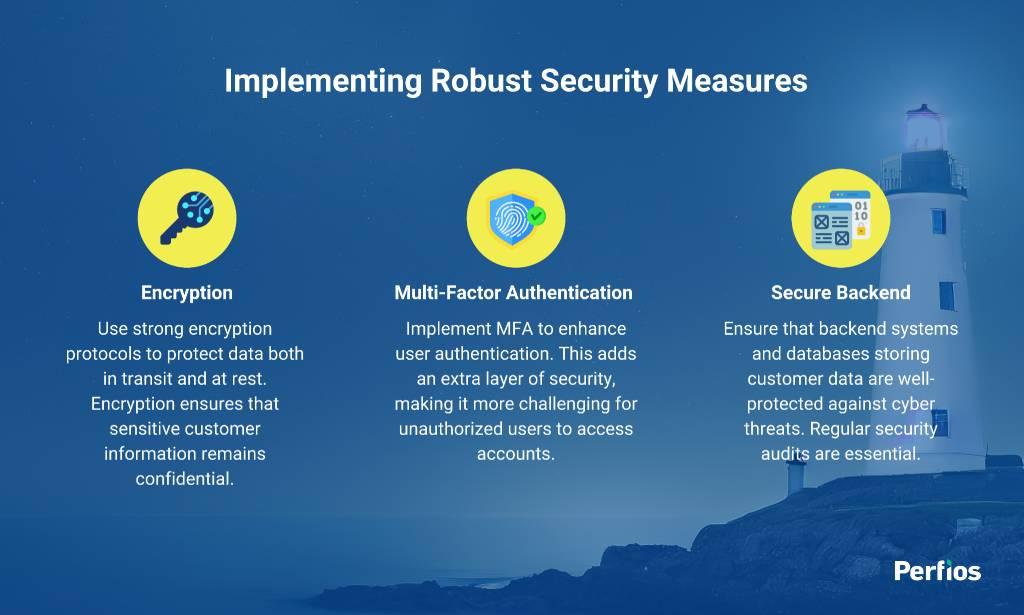

Security is paramount in mobile banking applications, and compliance plays a critical role in ensuring that customer data is protected. Here are some security measures to consider:

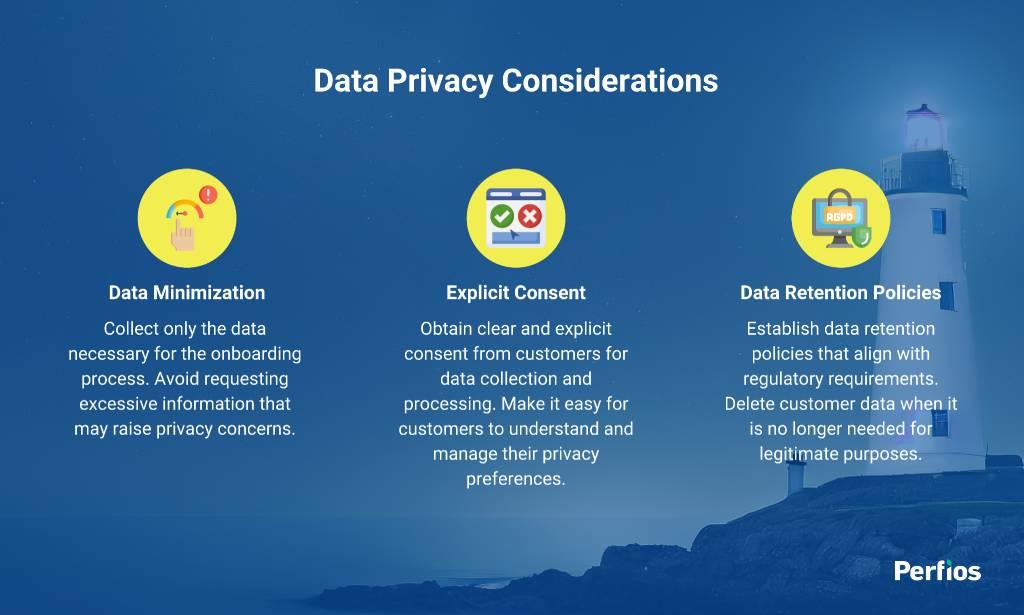

Data privacy is a significant concern for customers, and compliance with data protection laws is non-negotiable. Here's how to address this aspect:

One of the fundamental aspects of compliance in the banking sector, especially in mobile banking, is the precise identification and verification of customers through an onboarding customer API. The aim is to establish the authenticity of the individuals or entities using the banking services, safeguarding against fraud, money laundering, and other illicit activities.

This section will delve into the critical processes and considerations involved in customer identification and verification.

Accurate customer identification is the first line of defense against financial crimes. It ensures that banks know who their customers are and can assess the associated risks effectively. Here's why it's crucial:

● Fraud Prevention: Accurate identification helps in preventing identity theft and fraudulent account openings, protecting both the bank and its customers.

● AML Compliance: AML regulations require banks to verify customer identities as part of their due diligence. Non-compliance can result in legal penalties and reputational damage.

● Risk Assessment: Knowing your customer allows banks to assess the risk associated with each account. High-risk customers may require enhanced due diligence.

Collecting and verifying customer documents is a core part of the identification process. This typically includes:

● Government-Issued ID: Customers are usually required to provide a government-issued identification document such as a passport or driver's license.

● Proof of Address: Banks often request documents like utility bills or bank statements to confirm the customer's address.

● Biometric Data: Biometric data, such as fingerprints or facial recognition, can be used for identity verification, providing an extra layer of security.

Utilizing Optical Character Recognition (OCR) technology, Perfios significantly streamlines the document collection and extraction processes, thereby reducing friction in applications. Their industry-leading KYC OCR API is adept at recognizing and extracting data from a wide array of Officially Valid Documents (OVDs), including password-protected PDF files, which saves time and eradicates manual errors.

Biometric authentication methods are gaining prominence in mobile banking due to their accuracy and security. These include:

● Fingerprint Recognition: Using fingerprint sensors on smartphones to verify the customer's identity.

● Facial Recognition: Scanning the customer's face for authentication purposes, often using the phone's front camera.

● Voice Recognition: Analyzing the customer's voice for authentication, which is less common but gaining traction.

In the dynamic and highly regulated landscape of mobile banking, reporting and auditing are essential components of a robust compliance framework. These processes serve as checks and balances, ensuring that a bank's operations align with regulatory requirements and best practices. Let's delve into the significance of reporting and auditing in the context of mobile banking compliance.

Regular compliance reporting is a fundamental practice that banks must adhere to. It involves the systematic collection and analysis of data related to various compliance activities. The key aspects of compliance reporting in mobile banking include:

● Transaction Monitoring: Banks need to monitor customer transactions for any unusual or suspicious activities, which may indicate potential money laundering or fraud. Regular reports detailing these activities are essential for compliance.

● Customer Due Diligence (CDD): Reporting on CDD activities, including customer risk assessments, periodic reviews, and enhanced due diligence for high-risk customers, helps ensure that the bank is meeting regulatory requirements.

● Data Privacy and Security: Banks must report on data privacy and security measures, including breaches and incidents, to comply with data protection laws and maintain the trust of their customers.

● AML (Anti-Money Laundering) Compliance: Reporting on AML activities, including suspicious activity reports (SARs) and compliance with AML regulations, is crucial for demonstrating adherence to regulatory standards.

Internal and external audits play a pivotal role in ensuring that a bank's mobile banking operations are compliant and secure. These audits provide an independent assessment of the bank's practices and highlight areas that require improvement. Here's how they are typically conducted:

● Internal Audits: Banks should have internal audit teams or third-party auditors who periodically assess compliance with policies, procedures, and regulatory requirements. Internal audits help identify weaknesses and areas for improvement within the bank's compliance program.

● External Audits: Regulatory authorities and external audit firms may conduct audits of banks to assess their compliance with applicable laws and regulations. These audits are usually more comprehensive and serve as a critical external validation of a bank's compliance efforts.

● Corrective Action and Remediation: Audits often result in findings and recommendations for improvement. Banks are expected to take corrective action promptly and implement remediation plans to address identified deficiencies.

Reporting and auditing are integral components of maintaining compliance in mobile banking. They not only help banks meet regulatory requirements but also enhance the overall security and trustworthiness of their mobile banking services. Continuous vigilance and a commitment to improvement are essential in this ever-evolving landscape.

The modern banking landscape is characterized by rapid digitization, with mobile applications serving as the primary channel for customer interactions. This digital transformation has brought convenience and accessibility to banking services, but it has also introduced new challenges in terms of regulatory compliance. A key component in addressing these challenges is the integration of an Onboarding Customer API, which facilitates user-friendly onboarding while ensuring adherence to compliance standards.

Throughout this guide, we've highlighted the significance of a robust compliance framework, which encompasses a deep understanding of key regulations such as KYC, AML, and CDD. We've also explored the roles of international and local regulatory bodies like FATF, OCC, and GDPR in shaping compliance standards for mobile banking.

Mobile app development and compliance go hand in hand. The design of user-friendly onboarding processes, implementation of robust security measures, and meticulous attention to data privacy are essential elements that bridge the gap between user experience and compliance requirements.

As we move forward, it is essential for banks to remain vigilant, adapt to evolving regulations, and continue to invest in compliance measures that align with best practices. By doing so, they can offer their customers a secure, user-friendly, and compliant mobile banking experience that stands up to the highest standards of the financial industry.

Perfios Software Solutions is India’s largest SaaS-based B2B fintech software company enabling 900+ FIs to take informed decisions in real-time. Headquartered in mumbai, India, Perfios specializes in real-time credit decisioning, analytics, onboarding automation, due diligence, monitoring, litigation automation, and more.

Perfios’ core data platform has been built to aggregate and analyze both structured and unstructured data and provide vertical solutions combining both consented and public data for the BFSI space catering to their stringent Scale Performance, Security, and other SLA requirements.

You can write to us at connect@perfios.com

For more Such information contact us@ https://solutions.perfios.com/request-for-demo